Given that savings made relaxed expenditures more costly to possess People in america for the past while, it’s got a confident effect on home values. Based on home lookup business CoreLogic, an average Western resident had over $274,000 for the guarantee at the beginning of 2023. One to figure signifies an excellent $182,000 improve once the through to the pandemic.

Of numerous homeowners standing on eg tall sums away from family guarantee are tapping into you to guarantee for cash for different motives, anywhere between merging large-desire obligations to help you resource house home improvements. Yet not, the financing and you may credit product boasts a specific number of risk, and you may domestic guarantee funds and you may home equity personal lines of credit (HELOCs) are not any exceptions.

Uncertain if or not you really need to collect collateral out of your home? I requested particular gurus in the while using the your property collateral can get or is almost certainly not beneficial. If you’re considering using family collateral upcoming start by examining the latest prices might be eligible for right here.

Whenever borrowing out of your home equity is a good idea

Making use of your home guarantee tends to be advisable after you use it to improve your financial condition, particularly on the following conditions:

Making big renovations

Systems for example restorations your kitchen or incorporating a different sort of room is boost your residence’s overall worth. According to Irs, you can also meet the requirements in order to deduct the interest fees for individuals who make use of the loans to order, make or drastically alter your house.

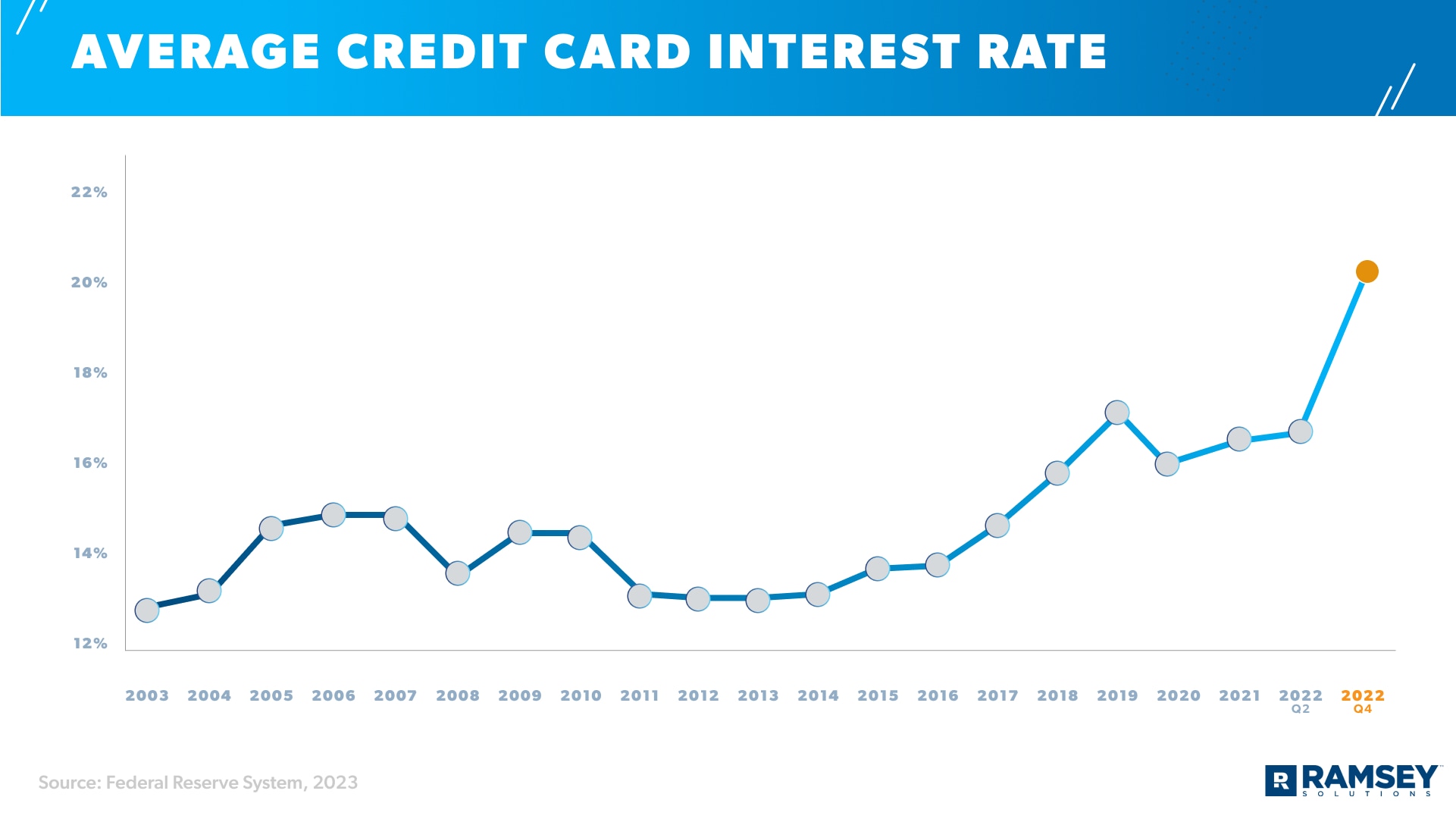

Sarah Alvarez, vp off home loan financial during the William Raveis Home loan, suggests HELOCs over the other loan choice. “As opposed to creating a cash-away refinance in the a high-price sector and you will probably shedding a 2%, 3% or 4% rate on your own first mortgage, you could just take an effective HELOC because subordinate capital so you’re able to tap new extra value of your house.”

Spending money on higher education

“Certain figuratively speaking, specifically loans for scientific otherwise rules school, can have quite high rates of interest,” says Doug Carey, CFA and inventor away from WealthTrace. “If you have high family equity, using it to finance training costs yourself or a household associate would be a cost-active option compared to high-attract student loans.”

Of course, it is wise to deplete their government education loan solutions in advance of flipping so you can personal loans or domestic guarantee things to the defenses they bring, including income-inspired repayment arrangements, deferment plus the prospect of student loan forgiveness.

Merging higher-notice debt

Domestic guarantee fund and you may HELOCs routinely have rather all the way down interest levels than handmade cards, thus combining their large-interest debt can lead to down monthly payments and desire fees. “This can help you perform loans and save money over the years,” says Carey.

When borrowing from the bank from your home security tends to be an awful idea

If you find yourself your residence guarantee can be a convenient means to fix supply cash for various objectives, either it’s not a wise alternative, and additionally within these factors:

Spending on nonessential motives

“It is far from a smart idea to end up being tempted to make use of house security to own frivolous requests,” says Ian Wright, director from the Team Capital. “Risking your property with regard to credit money to possess a good adore vacation otherwise updating your car or truck is unquestionably a dumb move.”

Credit from the large rates of interest

It may not getting smart to pull out financing otherwise personal line of credit “whether your credit payday loans Bessemer will not qualify your for the best HELOC or family equity financing,” recommends Michael Micheletti, captain telecommunications officer at the Open Tech. “We are enjoying even more borrowing firming, to manufacture they more challenging having property owners to be eligible for mortgage activities.”

Scraping equity needlessly

Utilizing your difficult-acquired equity may not be best in the event the you will find finest alternatives offered. “Such, figuratively speaking may be a much better choice to buy college or university according to rates and you may facts,” states Kendall Meade, an official financial coordinator within SoFi.

A method to make use of your house equity

- Family security loan: Typically, home guarantee money come with a fixed price and invite your to help you use a lump sum of cash. These fund make use of your domestic since security so you’re able to hold the financing.

- Household equity personal line of credit (HELOC): Much like credit cards, that it rotating credit line allows you to borrow funds as needed as much as their approved restriction.

- Cash-aside refinance: Having a funds-aside re-finance , your improve your current home loan with a new, larger that-preferably which have a lower life expectancy interest rate. You could pouch the difference from inside the cash within closure and employ it for pretty much people court objective.

- Opposite Mortgage:Contrary mortgage loans are made to help seniors decades 62 and you can elderly transfer the their home guarantee towards the bucks.

Analysis homework before proceeding which have one mortgage or borrowing from the bank equipment, due to the fact per is sold with its very own experts and you can cons. Find out more about your property collateral loan and you can HELOC possibilities here now.

The conclusion

Lenders generally require you to features at the very least 15% to help you 20% security so you can qualify for a house equity financing otherwise HELOC . When you yourself have large collateral in your home, you could potentially contemplate using a few of it in order to combine large-focus personal debt, renovate your residence and other objective. Think about, not, these types of collateral options are next mortgage loans which can be collateralized by your household, if you don’t build your monthly installments the need, it could lead to property foreclosure.